Tesla under pressure of falling margins. Are we expecting more declines?

Despite the correction of recent weeks, 2023 is a great success for Tesla. The stock is up 85% since the start of the year and some believe it may still be attractive as a long-term investment. So let's take a look at Tesla.

We've been warning about Tesla's earnings results for a long time. The most watched indicator, besides the number of cars delivered and produced, is the margin. And that has been severely compromised by Tesla's pricing policies. Indeed, Tesla has logically fought lower demand by getting cheaper, several times. So for Q3, we expected a significant margin reduction, which was finally confirmed.

Operating margin fell to 7.6%, compared to 17.2% a year ago. Moreover, for the first time since Q2 2019, Tesla missed market expectations for both profit and revenue. The stock reacted to the results with a big sell-off. In addition, Elon Musk expressed concern about the overall state of the global economy due to high-interest rates and expressed his intention to produce cheaper cars.

Tesla shares on D1 chart, MT4

Tesla, however, has two aces up its sleeve. The first is a new planned factory in Mexico, where construction was already due to begin. That should help Tesla produce even more cars at lower costs.

The second is the long-announced Cybertruck. The first cars should be delivered to customers at the end of November. But the question mark hangs over the price tag. It should be around $70,000 for the two-motor version, well below the market average for electric pickups in the US. This would confirm Elon Musk's words about a more affordable pricing policy. Moreover, the Cybertruck should be a literal hit, with almost 2 million people having confirmed their interest and a waiting period of up to 5 years.

Just for comparison, Tesla is expected to produce around 1.8 million new cars in the full year 2023. However, given the falling prices, Tesla's margins are likely to continue to suffer. The stock may thus be vulnerable to further sell-offs. However, the stock's fall below $200 may be used as a buying opportunity by some investors, and given the new production capacity and Cybertruck, Tesla may be interesting as a long-term investment.

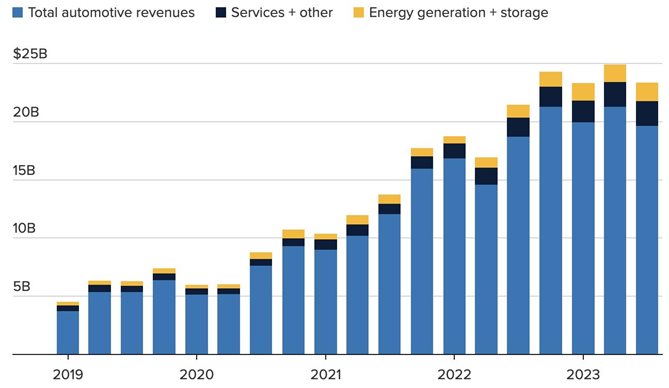

Tesla's quarterly sales by segment. Source: CNBC