Disney - a return to the limelight?

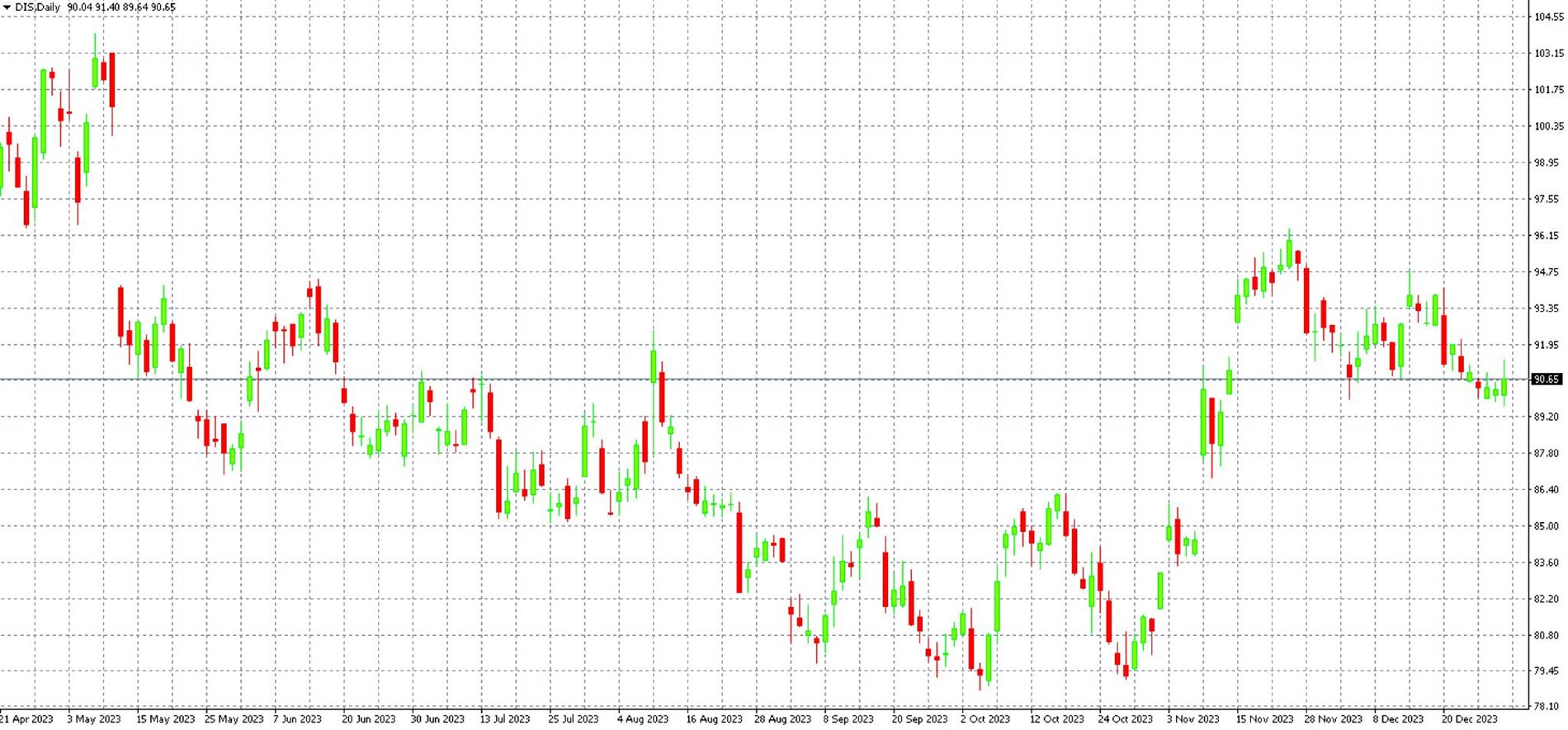

The year 2023 was one of the best for US stocks, with the S&P 500 index up more than 26% and the Nasdaq technology index up 43%. However, there was one famous name that did not experience any growth - Disney. Walt Disney shares ended 2023 with a gain of just 1.5%. Even though the start of the year 2023 was a dream come true for Disney, with the shares gaining 25% in January alone. However, as the year progressed, these gains were steadily eroded, falling to their lowest level in 9 years.

So what's the problem with Disney? The clouds are gathering over the theme parks in particular and also Marvel Studios. Both have been cash cows for Disney in the past. The theme parks were emptier than the company would have liked during the summer, especially the Florida park.

The problems at Marvel Studios have been glaring - the quality and sales of individual projects have steadily declined. Some films have barely ended up in black numbers, which is certainly not something Disney is used to after the blockbuster Avengers broke attendance and sales records in the past. The cost of new projects, however, is rather rising - the Secret Invasion series, for example, reportedly cost over $210 million, but reviews are inconsistent at best.

Disney currently reeks of desperation to deliver as much content as possible to its Disney+ platform in order to lure new subscribers. Disney and Marvel are now sort of paying the price for their past success - in the pre-pandemic era, the company sanctioned virtually every project because it saw virtually certain commercial success behind it.

Shares of Disney on D1 Chart, MT4

Disney was forced to make a turn due to circumstances. It has hired a new boss, Bob Iger, and laid off thousands of people to investigate. The latest quarterly results are already showing light at the end of the tunnel. The total number of Disney+ subscribers has already grown to 150 million, and the platform could finally report a profit by the end of this year. Total profits for the quarter were up 173% year-on-year and revenues were up 5%. Despite a weak summer, the theme parks have finally returned to prosperity and Disney plans to invest heavily in them over the next decade.

In addition, the new CEO is also succeeding in significantly reducing overall costs. The end of the strike in Hollywood could also help Disney, although it forced it to postpone several premieres. Overall, the next period will be one of transition for Disney and the stock may experience higher volatility in the short term. However, in the long term, Disney stock looks interesting and if the theme parks repeat their growth and manage to get the Disney+ platform into profit, the stock could very quickly return to the highs of last year.