The Swing Overview – Week 25

There was a rather quiet week in which the major world stock indices shook off previous losses and have been slowly rising since Monday. However, this is probably only a temporary correction of the current bearish trend. The CNB Bank Board met for the last time in its old composition and raised the interest rate to 7%, the highest level since 1999. However, the koruna barely reacted to this increase. The reason is that the main risks are still in place and fear of a recession keeps the markets in a risk-off sentiment that benefits the US dollar.

Macroeconomic data

We had a bit of a quiet week when it comes to macroeconomic data in the US. Industrial production data was reported, which grew by 0.2% month-on-month in May, which is less than the growth seen in April, when production grew by 1.4%. While the growth is slower than expected, it is still growth, which is a positive thing.

In terms of labor market data, the number of jobless claims held steady last week, reaching 229k. Thus, compared to the previous week, the number of claims fell by 2 thousand.

The US Dollar took a break in this quiet week and came down from its peak which is at 106, 86. Overall, however, the dollar is still in an uptrend. The US 10-year bond yields also fell last week and are currently hovering around 3%. The fall in bond yields was then a positive boost for equity indices.

Figure 1: US 10-year bond yields and USD index on the daily chart

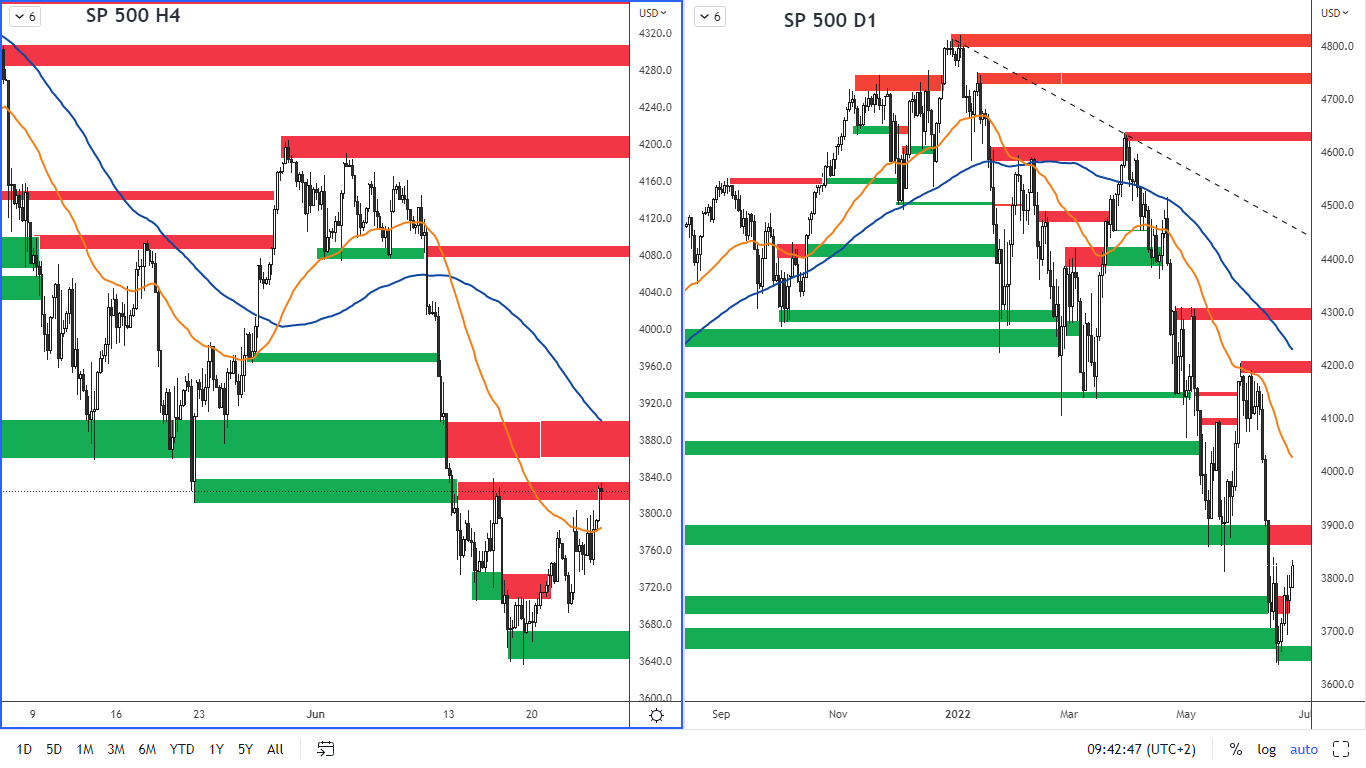

The SP 500 Index

The SP 500 index has been gaining since Monday, June 20, 2022. However, this is probably not a signal of a major bullish reversal. Fundamental reasons still rather speak for a weakening and so it could be a short-term correction of the current bearish trend. The rise is probably caused by long-term investors who were buying the dip. Next week the US will report the GDP data which could be the catalyst for further movement.

Figure 2: The SP 500 on H4 and D1 chart

The index has currently reached the resistance level according to the H4 chart, which is in the region of 3,820 - 3,836. The next strong resistance is then in the area of 3,870 - 3,900 where the previous support was broken and turned into the resistance. The current nearest support is 3 640 - 3 670.

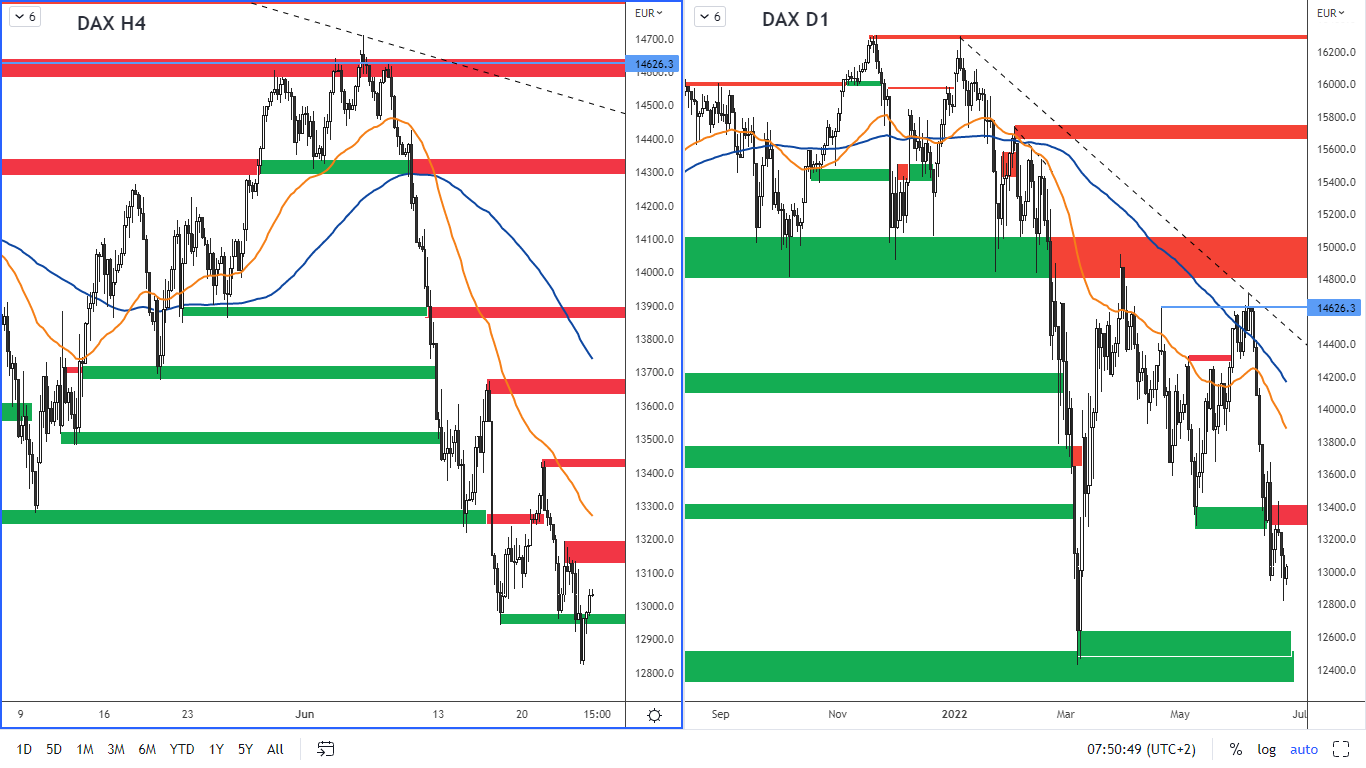

German DAX index

The manufacturing PMI for June came in at 52.0. The previous month's PMI was 54.8. While a value above 50 indicates an expected expansion, it must be said that the PMI has essentially been declining since February 2022. This, together with other data coming out of Germany, suggests a certain pessimism, which is also reflected in the DAX index.

Figure 3: German DAX index on H4 and daily chart

The DAX broke support according to the H4 chart at 12,950 - 12,980 but then broke back above that level, so we don't have a valid breakout. Overall, however, the DAX is in a downtrend and the technical analysis does not show a stronger sign of a reversal of this trend yet. The nearest resistance according to the H4 chart is 13,130 - 13,190. The next resistance is then at 13 420 - 13 440. Strong support according to the daily chart is 12,443 - 12,600.

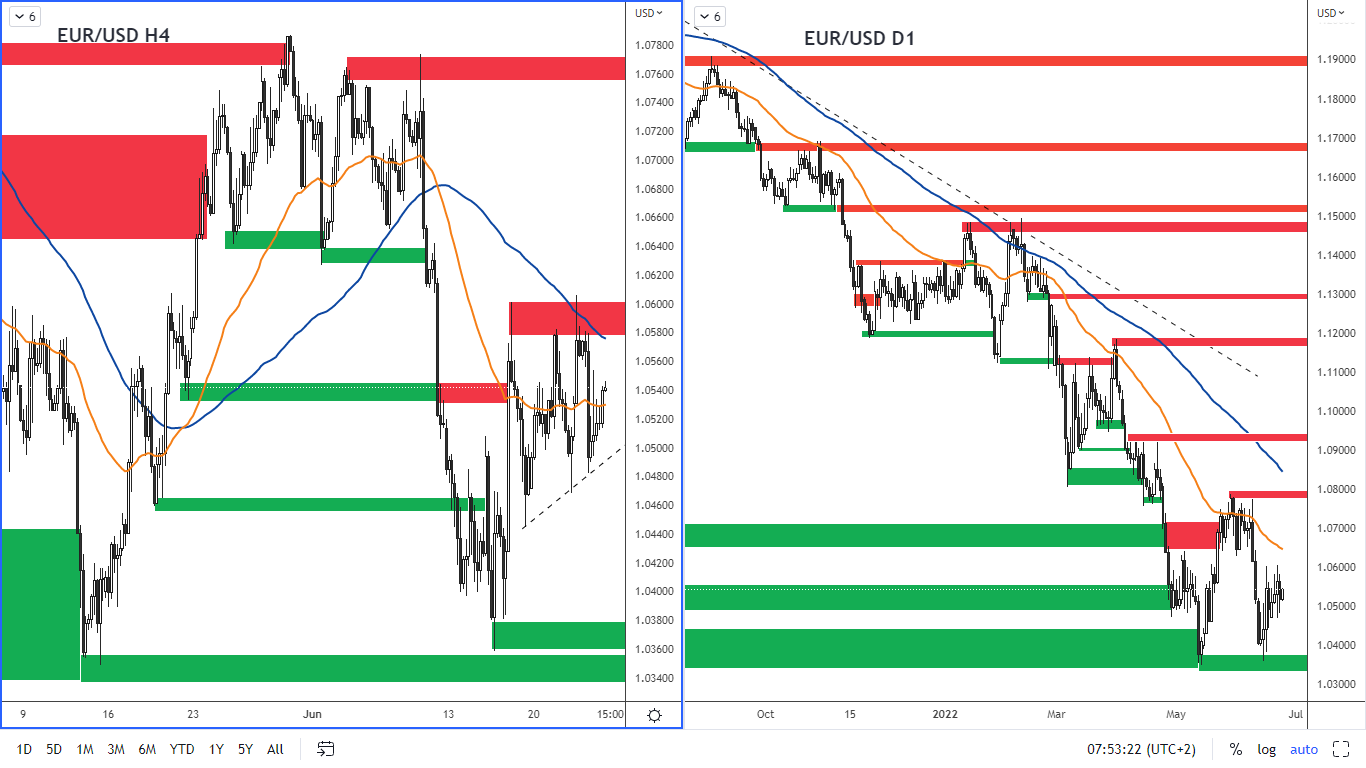

Eurozone inflation at a new record

Consumer inflation in the Eurozone for May rose by 8.1% year-on-year as expected by analysts. On a month-on-month basis, inflation added 0.8% compared to April. The rise in inflation could support the ECB's decision to raise rates possibly by more than the 0.25% expected so far, which is expected to happen at the July meeting.

Figure 4: EUR/USD on H4 and daily chart

From a technical perspective, the euro has bounced off support on the pair with the US dollar according to the daily chart, which is in the 1.0340 - 1.0370 range and continues to strengthen. Overall, however, the pair is still in a downtrend. The US Fed has been much more aggressive in fighting inflation than the ECB and this continues to put pressure on the bearish trend in the euro. The nearest resistance according to the H4 chart is at 1.058 - 1.0600. Strong resistance according to the daily chart is at 1.0780 - 1.0800.

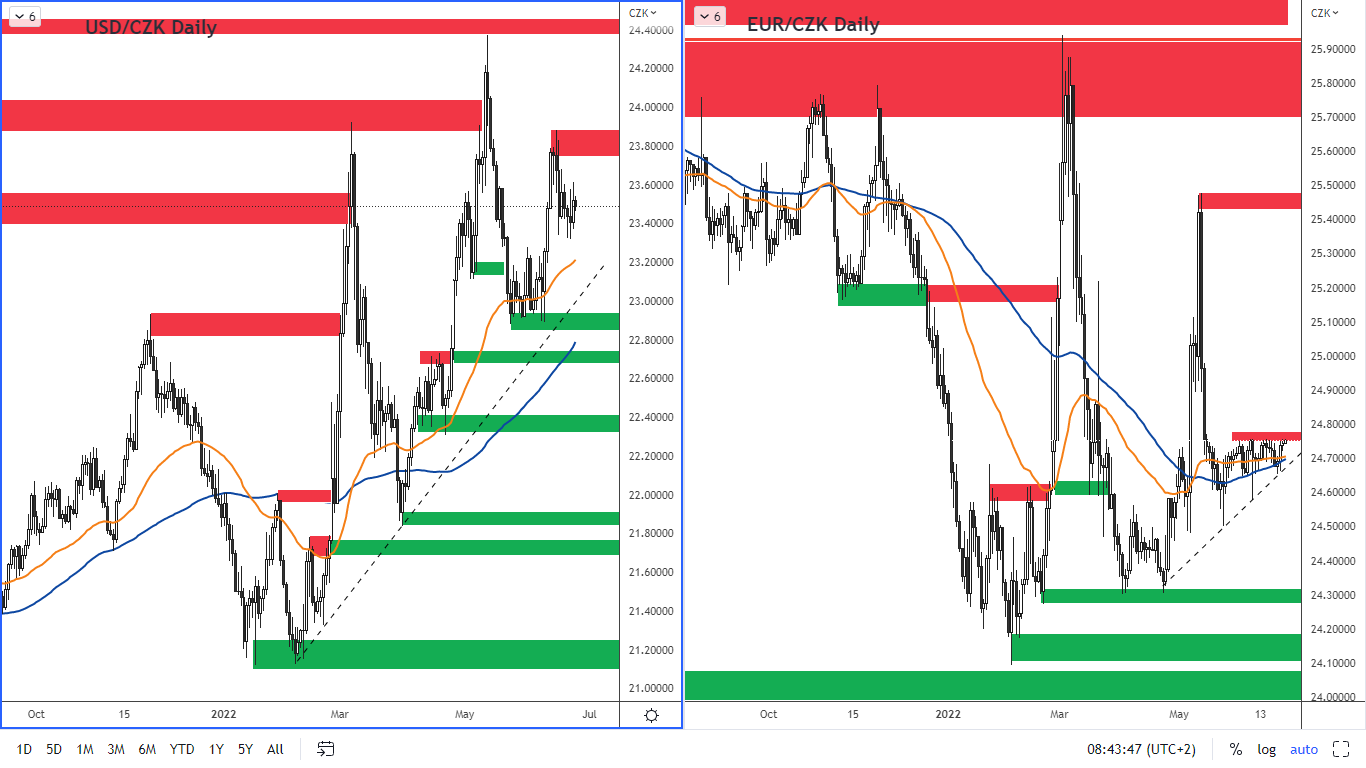

The Czech National Bank raised the interest rate again

Rising inflation, which has already reached 16% in the Czech Republic, forced the CNB's board to raise interest rates again. The key interest rate is now at 7%. The last time the interest rate was this high was in 1999. This is the last decision of the old Bank Board. In August, the new board, which is not clearly hawkish, will decide on monetary policy. Therefore, it will be very interesting to see how they approach the rising inflation.

The current risks, according to the CNB, are higher price growth at home and abroad, the risk of a halt in energy supplies from Russia and generally rising inflation expectations. The lingering risk is, of course, the war in Ukraine. The CNB has also decided to continue intervening in the market to keep the Czech koruna exchange rate within acceptable limits and prevent it from depreciating, which would increase import inflation pressures.

Figure 5: The USD/CZK and The EUR/CZK on the daily chart

Looking at the charts, the koruna hardly reacted at all to the CNB's decision to raise rates sharply. Against the dollar, the koruna is weakening somewhat, while against the euro the koruna is holding its value around 24.60 - 24.80.

The appreciation of the koruna after the interest rate hike was probably prevented by uncertainty about how the new board will treat inflation, and also by the fact that there is a risk-off sentiment in global markets and investors prefer so-called safe havens in such cases, which include the US dollar.