The Swing Overview - Week 13

Equity indices closed the first quarter of 2022 in a loss under the influence of geopolitical tensions. The Czech koruna strengthened as a result of the CNB raising interest rates to 5%, the highest since 2001. The US supports the oil market by releasing 180 million barrels from its strategic reserves.

War in Ukraine

The war in Ukraine has been going on for more than a month and there is still no end in sight. Ongoing diplomatic negotiations have not led to a result yet. Meanwhile, Russian President Putin has decided that European countries will pay for Russian gas in rubles. This has been described as blackmailing from Europe's point of view and is not in line with the gas supply contracts that have been concluded. A way around this is to open an account with Gazprombank where the gas can be paid for in euros. Geopolitical tensions are therefore still ongoing and are having a negative effect on stock markets.

Equity indices have had their worst quarter since 2020

US and European equities posted their biggest quarterly loss since the beginning of 2020, when the COVID-19 pandemic broke out and the global economy was in crisis. Portfolio rebalancing at the end of the quarter boosted demand for bonds and kept yields lower.

On Tuesday, the yield curve briefly inverted, meaning that short-term bonds yields were higher than long-term bonds. An inverted yield curve is a signal of a recession according to many economists. It means that future corporate profits should be rather behind expectations and stock prices might reflect it.

On Thursday, the S&P 500 index fell 1.6%. The Dow Jones industrial index also fell by 1.6% and the Nasdaq Composite index fell by 1.5%. The European STOXX 600 index closed down by 0.94%.

Even after last week's rally, as investors celebrated signs of progress in peace talks between Russia and Ukraine, the S&P 500 index is still down 5% for the first three months, its worst quarterly performance in two years.

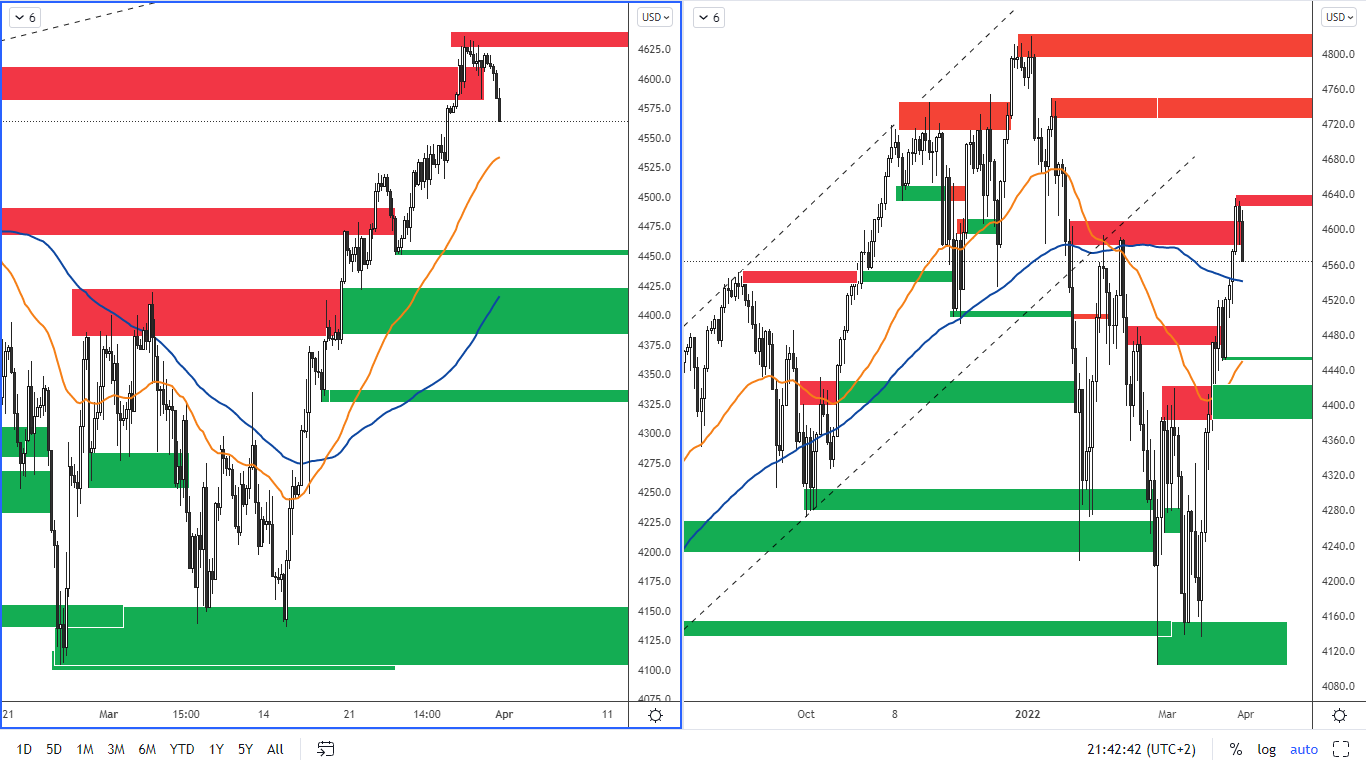

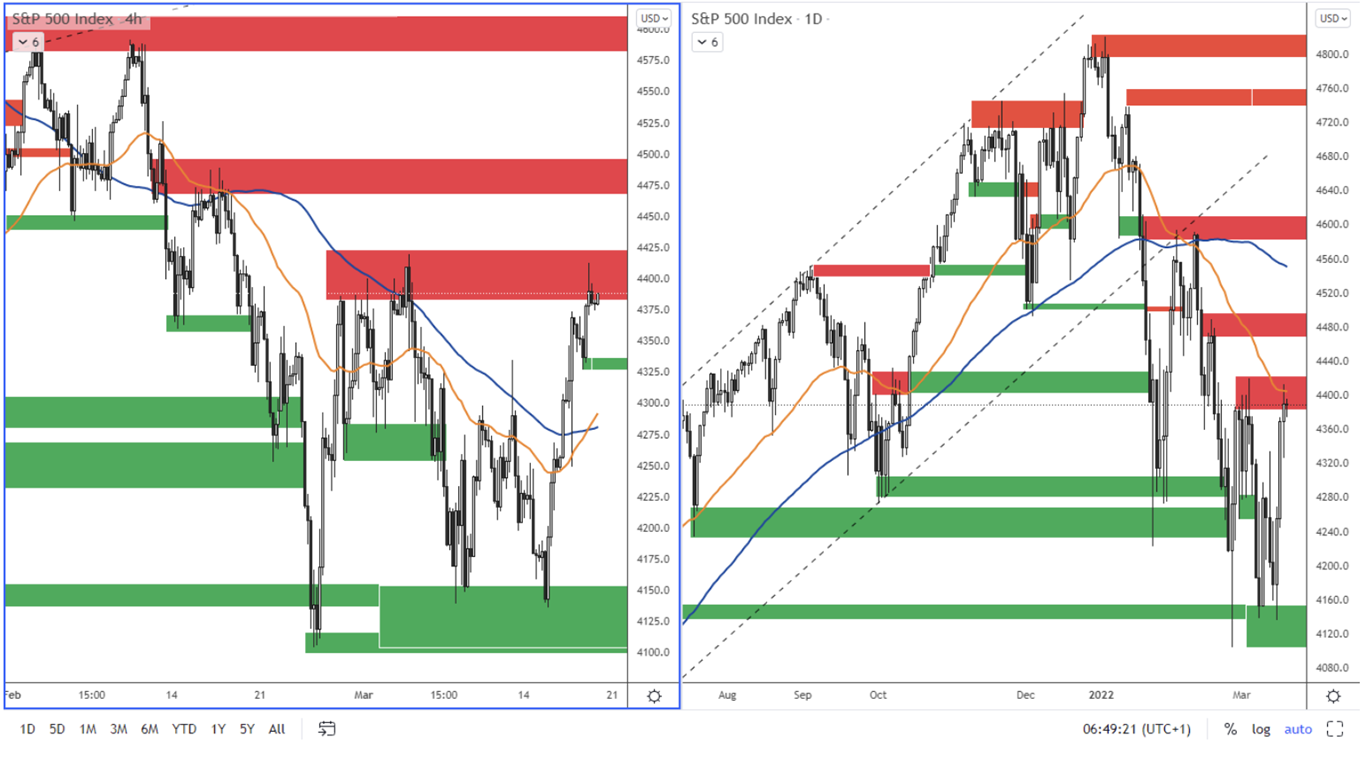

Figure 1: SP 500 on H4 and D1 chart

The SP 500 index reached the resistance level at 4,600, which it broke, but then closed below it. This indicates a false break. The new nearest resistance is in the range of 4,625 - 4,635. Support is at 4,453 and then significant support is at 4,386 - 4,422.

German DAX index

The DAX index has rallied since March 8 and has reached the resistance level which is in the 14,800 - 15,000 range. However, the index started to weaken in the second half of the week. The news that Russia will demand payments for gas in rubles, which Western countries refuse, contributed to the index's weakening. The fear of gas supply disruption then caused a sell-off.

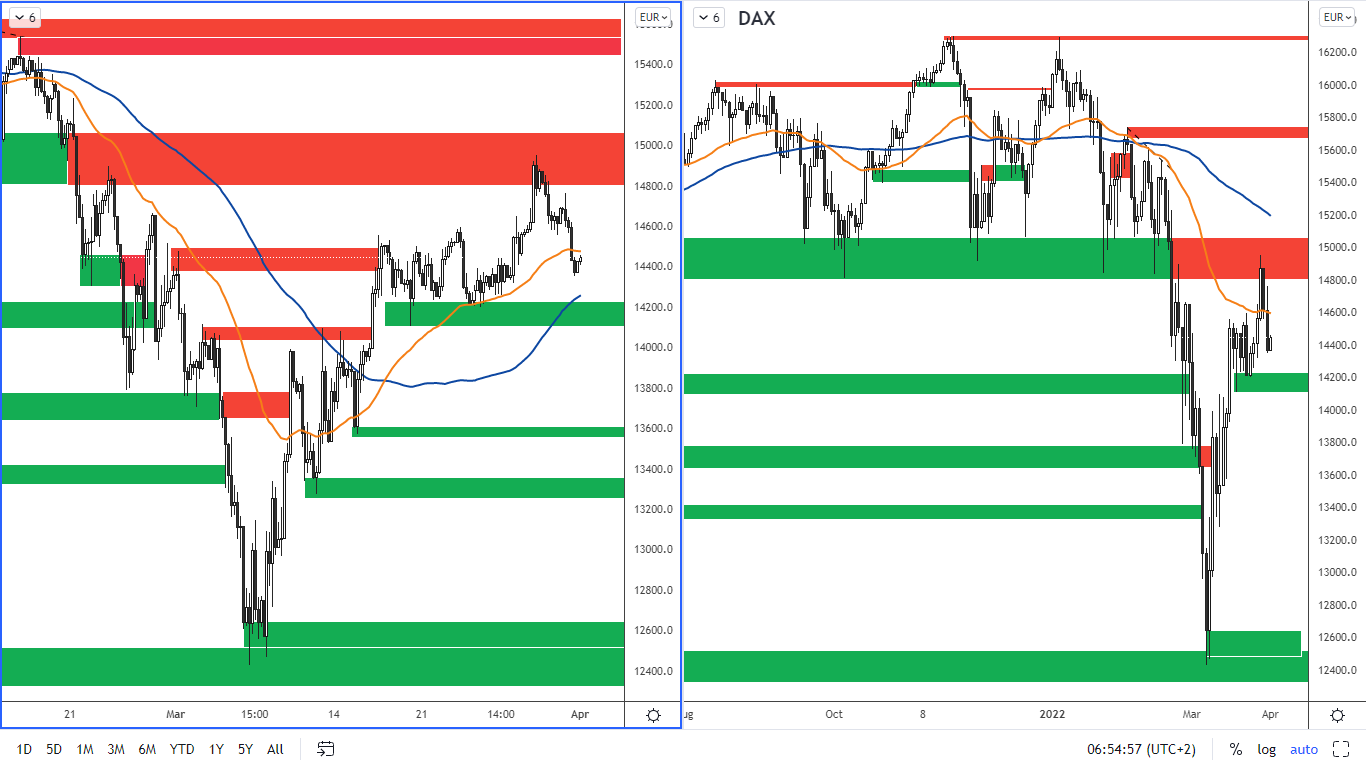

Figure 2: German DAX index on H4 and daily chart

Figure 2: German DAX index on H4 and daily chart

Resistance is between 14,800 - 15,000 according to the daily chart. The nearest support according to the H4 chart is at 14,100 - 14,200.

The euro remains in a downtrend

The euro was supported at the beginning of the week by hopes for peace in Ukraine. However, by the end of the week, the Ukrainian President warned that Russia was preparing for more attacks and the Euro started to weaken. News of Russia's demand to pay for gas in rubles had a negative effect on the euro as well.

Figure 3: The EURUSD on the H4 and daily charts.

Figure 3: The EURUSD on the H4 and daily charts.

From a technical point of view, we can see that the EURUSD according to the daily chart has reached the resistance formed by EMA 50 (yellow line). The new horizontal resistance is in the area of 1.1160 - 1.1180. Support is at 1.0950 - 1.0980. The euro still remains in a downtrend.

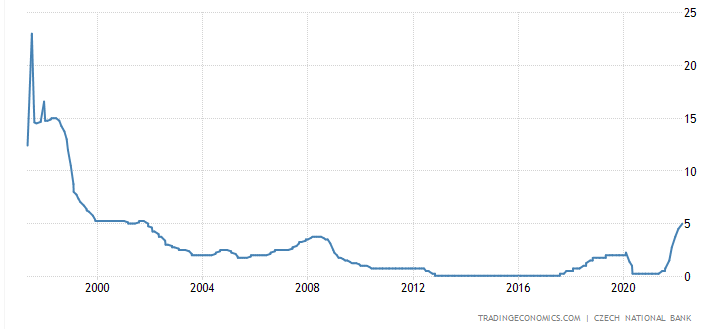

CNB raised the interest rate

In the fight against the inflation, the CNB decided to further raise the interest rate by 0.50%. Currently, the base rate is at 5%, where it was last in 2001. The interest rate hike is aimed at slowing inflation by slowing demand through higher borrowing costs.

Figure 4: Interest rate developments in the Czech Republic

Figure 4: Interest rate developments in the Czech Republic

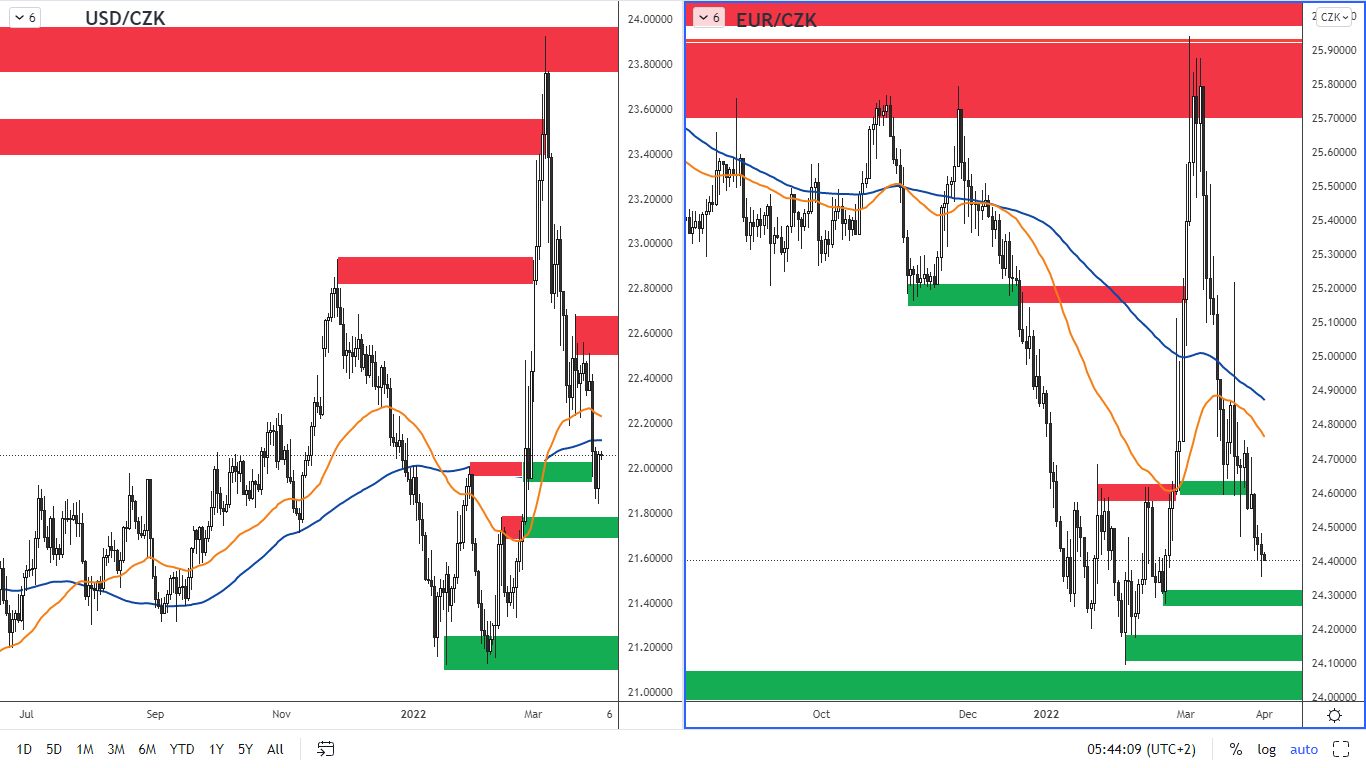

In addition, a strong koruna should support the slowdown in inflation. The koruna could appreciate especially against the euro due to higher interest rates. However, the strengthening of the koruna is conditional on the war in Ukraine not escalating further. We can see that the koruna against the euro is approaching a support around 24.30. The low of this year was 24.10 korunas for one euro.

Figure 5: USD/CZK and EUR/CZK on the daily chart.

Figure 5: USD/CZK and EUR/CZK on the daily chart.

The koruna is also strengthening against the US dollar. Here, however, the situation is slightly different in that the US Fed is also raising rates and is expected to continue raising rates until the end of the year. Therefore, the interest rate differential between the koruna and the dollar is less favourable than between the koruna and the euro. The appreciation of the koruna against the dollar is therefore slower.

Currently, the koruna is at the support of 22 koruna per dollar. The next support is at 21.70 and then 21.10 koruna per dollar, where this year's low is.

Oil has weakened

Oil prices saw the deep losses after the news that the United States will release up to 180 million barrels from its strategic petroleum reserves as part of measures to reduce fuel prices. US crude oil fell 5.4% and Brent crude oil fell 6.6% on Thursday after the news.

Figure 6: Brent crude oil on a monthly and daily chart

Figure 6: Brent crude oil on a monthly and daily chart

We can see that a strong bearish pinbar was formed on a monthly chart. The nearest support is in the zone 103 – 106 USD per barel. A strong support is around 100 USD per barel which will be closely watched.